2024 MORTGAGE FORECAST

Posted: March 11, 2024

The rate forecast projections I am relying on are from MBS Highway and Barry Habib from his annual forecast session we had in February 2024. I get access to this through one of my mortgage partners - Carrie Nash at Highlands Mortgage (whom I highly recommend).

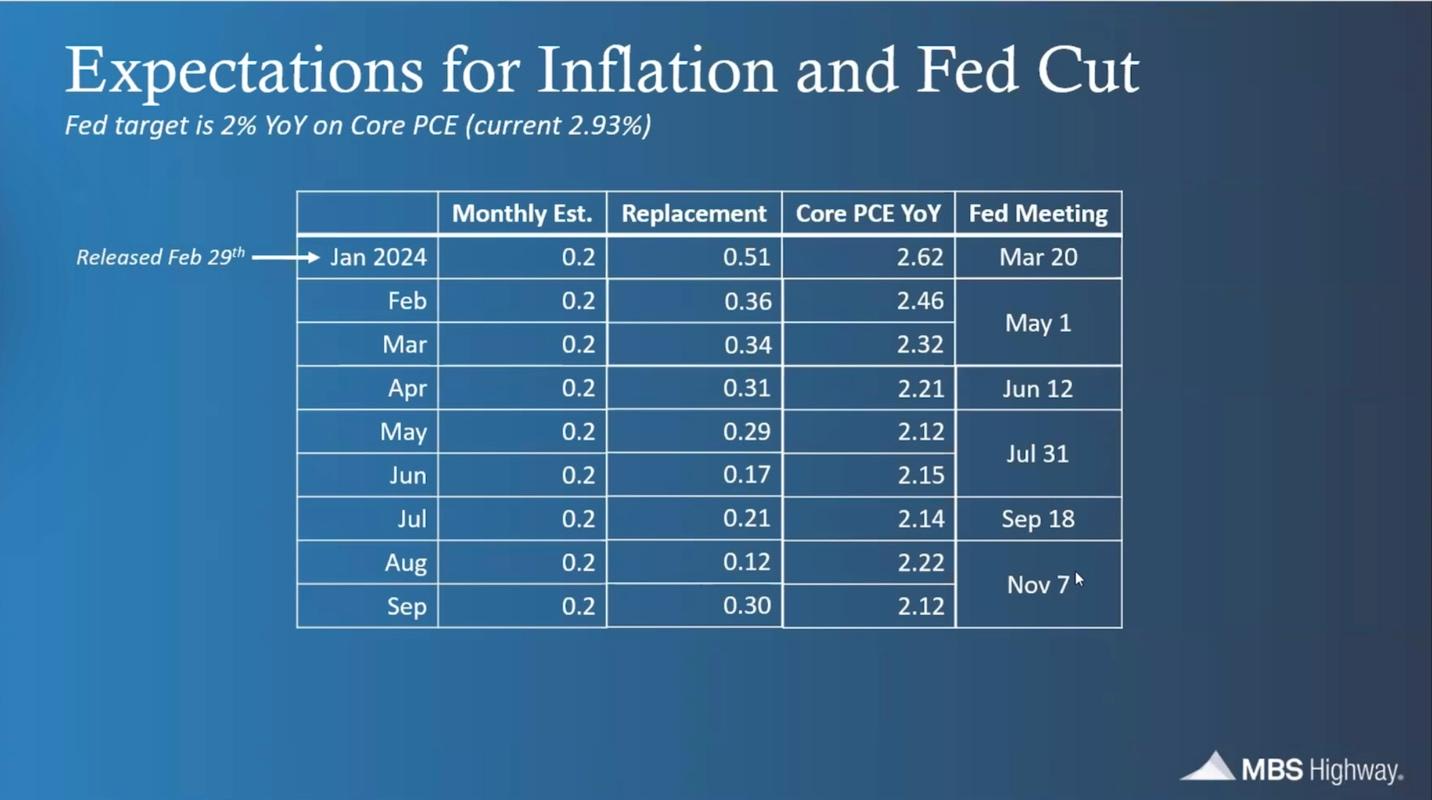

Barry is watching Core PCE (Personal Consumption Expenditure). This is a rolling 12 month average. As such - it lags behind the current monthly number and takes longer to come down. The new number replaces the number from 12 months ago, which allows us to (at least) know what number is being replaced, while also having a pretty good forecast of what new number will be coming in (based on trending data from month prior and other trends

Here is how those projections look, along with which Fed Meeting these numbers will be reported by:

The Fed Target is 2. So for March, a number of 2.62 isn't low enough to start easing the rates by performing a cut. But by May or June, the expected numbers are getting close enough to warrant a cut.

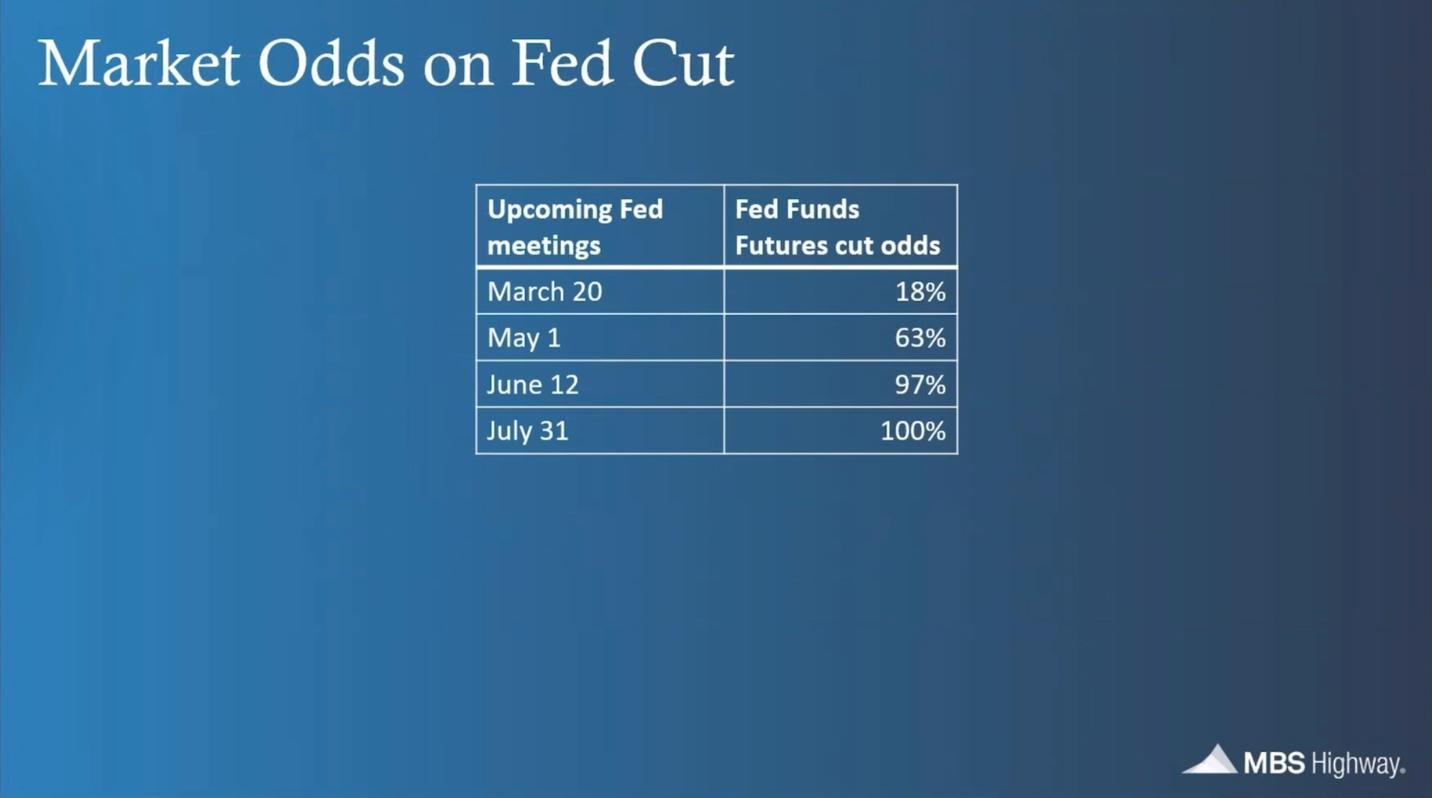

Wall Street also places odds on what they think will happen in the market, and Wall Street agrees that by May or June, we should start seeing rate cuts from the Fed:

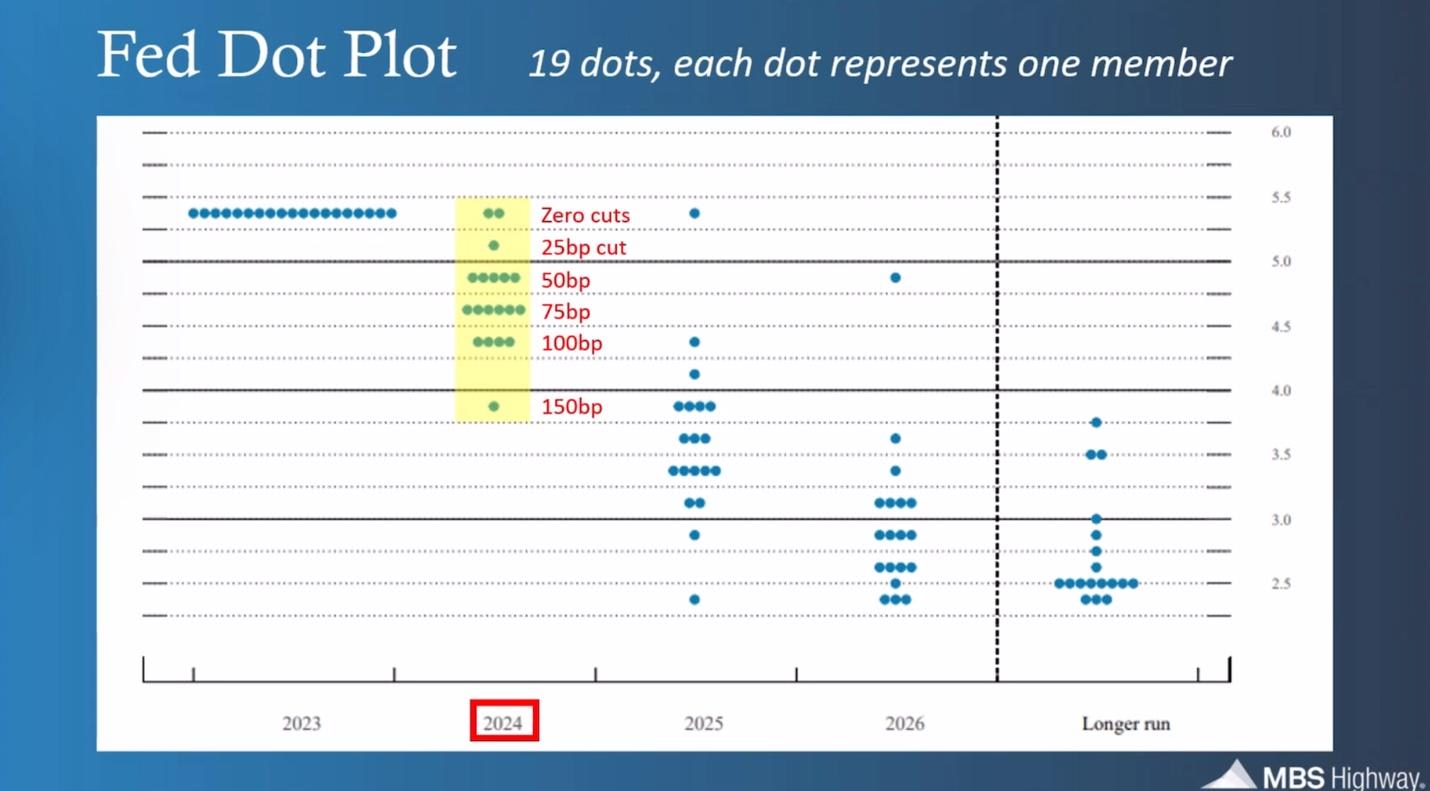

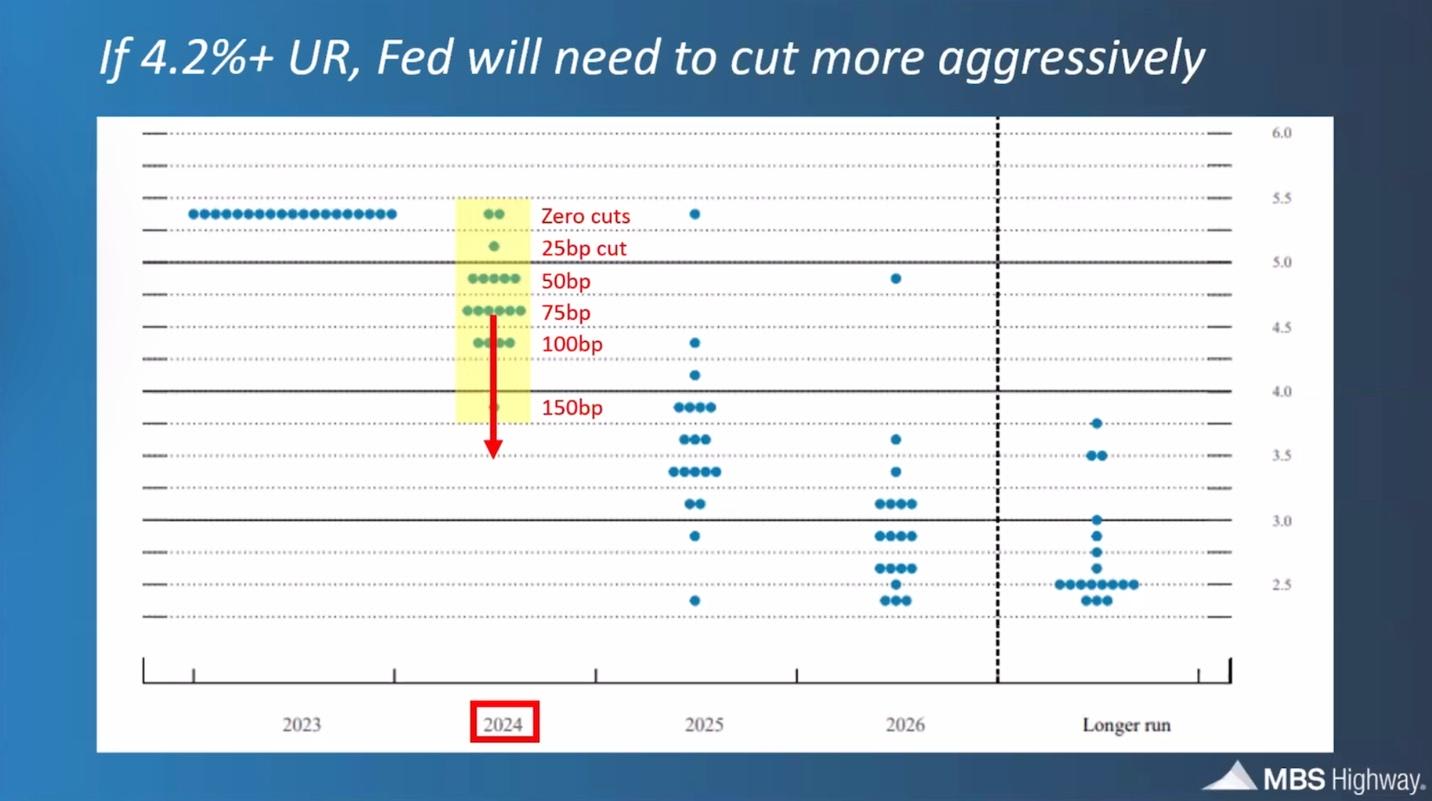

Further, is the Fed Dot Plot showing the forecast and expectation of each of the 19 Fed Reserve Members. Nobody expected cuts in 2023. 17 expect cuts in 2024 with 16 of them expecting 50 basis point cut, or sometimes significantly more.

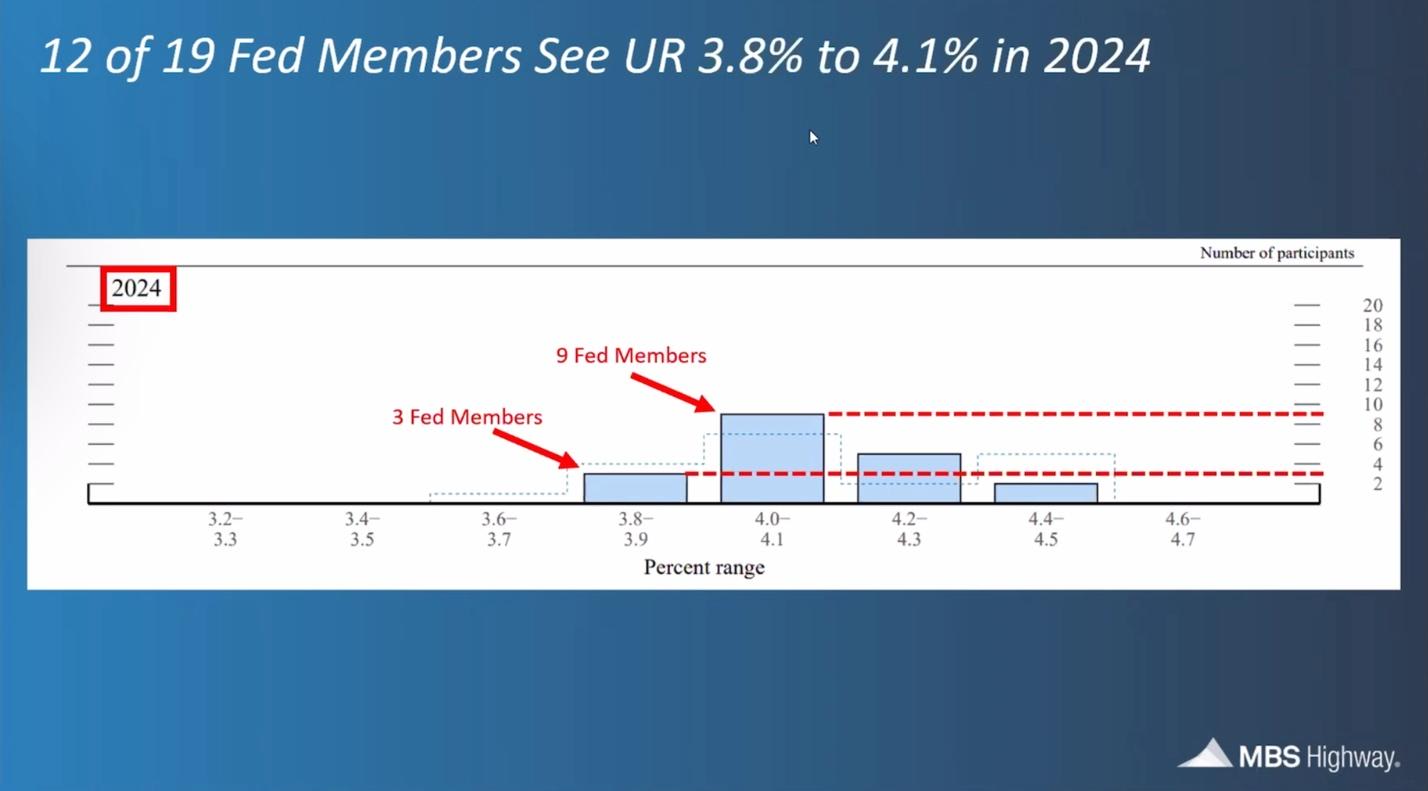

The above forecast is from the same members that expect the Unemployment Rate to stay relatively low. Current Unemployment is 3.7%. 12 Expect it raise slightly but to stay below 4.1. 7 of the members expect unemployment to rise a bit more.

If UR does raise more, they will likely be more willing to cut more:

Of course, if it stays at 3.7 or below, perhaps that gives them less reason to cut the rates. That said, the inflation data should still be supporting a rate cut.

If rates come down, buyers will enter the market and prices will go up and we will start seeing more appreciation (back to the 40 year average of 6% a year, or more):

This all gives me confidence that the larger dynamics at play will continue to trend toward a sellers market in the late spring or early summer. Seasonally and pent up demand will come into play in the early spring. Interest Rates should help in the later spring.

Barry does this every year for us and he calls it as he sees it. I've watched him be pretty on point for the last 3 years.

ADVICE FOR HOME SHOPPERS

If you’re waiting for rates to come down before you become active in the market - This could actually be an opportunity to buy the home if you want to take advantage before buyer competition returns. Let’s connect today to explore the options in our local market.

Mortgage Rates are always changing. If you would like to know the current mortgage rates or would like any strategy to find affordability in the current mortgage rate market, please give me a call today!

STRATEGY

The most common strategy around Mortgage Rates in the current market is to negotiate a 2-1 Buydown.

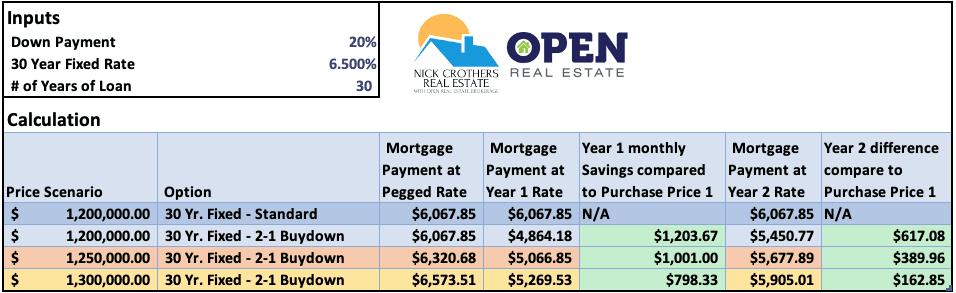

To show the advantages of a 2-1 Buydown, I have built this illustration. The essence is that the seller gives a concession to pay for a 2-1 buydown for the buyer. The buyer has a pegged payment based on current interest rates. But with the concession, the seller places money in escrow (a holding account) to subsidize the buyers’ payments by 2% less than the pegged rate in the first year and 1% less than the pegged rate in the second year. Here is the effect for the buyer:

As you can see, the 2-1 buy down would allow a buyer to save $1200 a month in the first year, or offer $100,000 more on a house in this example, while still saving ~$800 a month in the first year and ~$160 a month in the second year. The pegged rate is 6.5%, but the buyer is making a payment in the first year that is effectively 4.5%, and in the second year effectively 5.5%. The strategy here is that the buyer has an opportunity to refinance into a lower rate and has a 2-year runway to do so to maintain that monthly affordability.

The seller concession in this illustration is ~$22k-$23k depending on the purchase price. Thus, the buyer can offer that much more on their purchase price to make the seller whole and have a large monthly savings with a runway to refinance and retain some of that affordability long term.

OTHER THINGS TO KNOW:

- As the purchase price increases, so does the down payment. IE - it might allow you to get into a house with monthly affordability, but you will have to put more down if you want to keep the same down payment %. There are plenty of options to put less than 20% down on a home.

- The home still needs to be appraised. We aren’t having any issues with appraisals these days, but it could be a snag, and it is important to understand the possibility that if you offer slightly higher, it needs to appraise slightly higher.

- If the buyer refinances before the buydown funds are fully utilized, those funds go to the buyer. IE – there is no forfeiture of these funds if you have any opportunity to secure a lower fixed rate.

- In my opinion, this is a win/win. It allows the seller to sell the home quicker and for their required price (or close to it), and it gives the buyer affordability and a runway to operate with.

- This can allow a buyer to operate in a high-interest rate environment, gain affordability, and purchase while much of the buyer competition is on the sidelines. It does require the buyer to take on the risk that interest rates don’t come down and a refinance opportunity doesn’t present itself. That said, this is the ultimate strategy to employ with the mentality of “Dating the Rate, and Marrying the House”.

THIS IS A BASIC ILLUSTRATION OF THIS STRATEGY. THERE ARE OTHER OPTIONS AND STRATEGIES TO EMPLOY. PLEASE CALL ME TODAY AT (720) 955-8337 TO DISCUSS VARIOUS OPTIONS.